UK Retailer Index 2022

ATNI’s UK Retailer Index 2022 is the first full nutrition- and health-specific Index to assess all major food retailers within the UK market

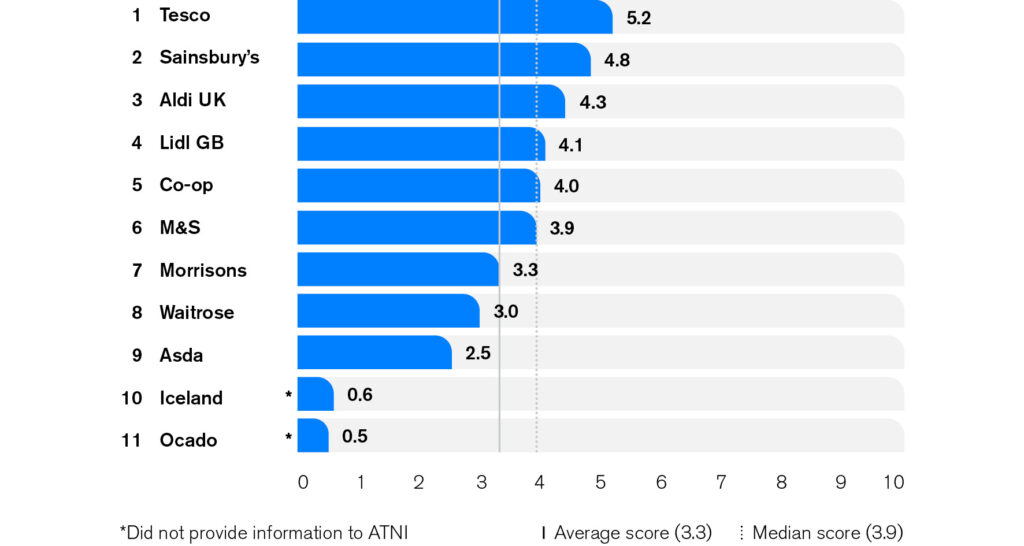

Ranking

The average score across all retailers is 3.3 out of 10

Methodology

How did we assess the retailers in this Index?

The UK Retailer Index 2022 consists of eight nutrition-related Topics, which are based on the Categories within ATNI’s Global Index and which have been developed in consultation with UK experts. The UK Supermarket Spotlight 2020 was the precursor to the UK Retailer Index 2022 and provided clear proof of concept: the current Index refines and significantly expands on the Spotlight report. ATNI actively sought engagement with all 11 retailers at several points in the assessment process (including through the use of non-disclosure agreements) to ensure that the analysis and reporting is as detailed, fair and representative as possible.

Each retailer was assessed in mid-2021 by ATNI on a total of 126 indicators, covering commitment, performance and disclosure across the Topics. Together, the Topics address governance, the production and placement of healthy, affordable products, and how the retailers influence customer choices and behaviour, both online and in-store. Each Topic is weighted according to the impact that it is considered to have on the diet of the retailers’ customers across the UK.

Retailers

Click on the retailer's logo to open their Scorecard

Go to company scorecard

Go to company scorecard

Go to company scorecard

Go to company scorecard

Go to company scorecard

Go to company scorecard

Go to company scorecard

Go to company scorecard

Go to company scorecard

Go to company scorecard

Go to company scorecard

Acknowledgements

| The ATNI UK Retailer Index 2022 is being supported by ShareAction, through a grant from Impact on Urban Health, part of Guy’s & St Thomas’ Foundation.

|

The writing of this ATNI UK Retailer Index 2022 report, the underlying methodology development and the research were conducted by the Access to Nutrition Initiative UK Retailer Index project team, which consists of Martina Asquini, Babs Ates, Marije Boomsma, Inge Kauer, Nadine Nasser, Aurélie Reynier, Elena Schmider, Alex Tobin and Mark Wijne, along with external consultants Katy Cooper (lead author) and Mali Gravell.

ATNI wishes to thank our UK Retailer Index expert group members Chris Holmes, Mike Rayner and Christina Vogel for their valuable input and advice throughout the development of this report and underlying methodology. We would also like to thank Ignacio Vazquez and Lily Roberts from ShareAction, who contributed to improving the report.

Design & formatting: Kummer & Herrman