Materiality of Nutrition

Are financial markets missing the value of healthy foods?

Project Overview

An unhealthy diet is the leading global cause of disease, disability, and premature death, and one of the top two risk factors for non-communicable diseases (NCDs). In addition to the health-related consequences of malnutrition, it increases risks and costs to employers across all sections of the economy.

On average, across the 52 OECD countries, 8.4% of the health budget is expected to be spent to treat the consequences of overweight between 2020 and 2050, with the associated average reduction in GDP due to lower employment and reduced productivity predicted to be 3.3%, accompanied by a reduction in average life expectancy of three years. The expected economic costs of undernutrition, in terms of lost national productivity and economic growth, range from 2% to 3% of GDP in some countries, up to 11% of GDP in Africa and Asia each year.

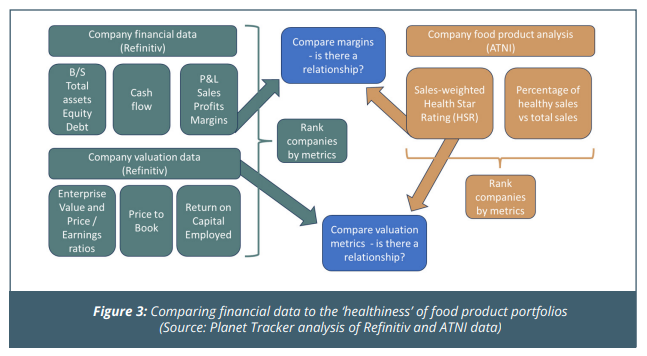

Given the health and economic impact of unhealthy diets, the Access to Nutrition initiative (ATNi) in collaboration with Planet Tracker undertook research on the materiality of nutrition, which aimed to identify if investors were missing economic opportunities by not investing intentionally in companies with healthier food portfolios.

This research compared the healthiness of 20 global food manufacturers’ food product portfolios with their profits and market valuations. The total revenue for the included companies was worth USD 6.6 trillion in 2022 (10% of the total food and beverage market). An additional analysis was conducted on a subset of the company’s annual reports and earnings call transcripts to identify the extent to which companies and/or investors were discussing the healthiness of food product portfolios.

Read the executive summaryMethodology

The challenge of a small sample: grouping to compare like-with-like

For this research on the materiality of nutrition, information for the healthiness of global food portfolios was based on health star rating data provided by ATNi’s Global Access to Nutrition Index, while company-reported financial and valuation data were taken from Refinitiv.

Given the relatively small and diverse sample of 20 F&B manufacturing companies covered by the 2021 ATNi Global Index, the extent of statistical analysis was limited. To address this challenge, the companies were categorised into four distinct groups based on market capitalisation and the breadth of their food portfolios: smaller vs. larger companies, and narrower vs. broader portfolios. Each group was further analysed based on their Health Star Ratings (HSR), distinguishing between ‘healthier’ (HSR ≥ 2.5) and ‘unhealthier’ (HSR ≤ 2.3) portfolios. This grouping aimed to facilitate more accurate like-for-like comparisons, although it did not yield equally sized categories across the divisions.

The categorisation process revealed trends within the sample, including the distribution of companies based on market cap and food category count. However, the small sample size posed challenges, as some sub-groups contained only one company, raising the risk of distorted results due to the influence of outliers. Overall, while the methodology aimed to provide a structured analysis, the findings should be interpreted with caution due to the limitations associated with the sample size and the diversity of the companies involved.

Read the full report here